|

Commentary |

|

Stock bulls are hoping stellar earnings results from both Microsoft and Google-parent Alphabet can get the rally back on track today.

The results, released after the market close, sent stock shares of both companies higher in after hours trading. Notably, both firms reported growth in their cloud divisions that they each attributed to new AI tools. Microsoft’s Azure growth was more than +30% while operating income in Google’s cloud biz more than quadrupled. However, there were also some pretty big earnings disappointments yesterday, including IBM, Intel, and Caterpillar, which continues the same “mixed” trend seen so far from Q1 2024 earnings results.

Stock bulls also continue to face headwinds from economic data that shows inflation heading the wrong direction. The first estimate of Q1 GDP (gross domestic product) yesterday showed inflation was much-stronger-than-expected. The inflation component, the so-called “PCE Deflator” (also one of the Fed's preferred inflation measures) was expected to accelerate to +2.8% from +1.6% in Q4 2023 but came in substantially hotter at +3.4%. At the same time, growth was slower-than-expected at just +1.8% versus Wall Street’s estimate of around +2.4%.

The combination of rising inflation and slowing growth is renewing worries that the US economy could be headed toward “stagflation”. Most economists consider stagflation, aka low-to-no economic growth and persistent inflation, to be one of the worst outcomes for any economy, topped only by “depression”.

Stagflation also is one of the least preferred outcomes by companies and Wall Street as well because it’s just incredibly tough for anyone to make a profit in a high-margin/low-sales environment. Keep in mind, this is the first estimate of Q1 2024 GDP and the PCE Deflator. There are two revisions to come that could see those numbers shift in more favorable directions. Investors today will get another look at March inflation from the PCE Prices Index, also a Fed favorite.

Wall Street expects the headline rate to increase slightly to +2.6% from +2.5% year-over-year and the “core” rate (strips out food and energy) to decline a bit to +2.7% from +2.8% in February.

Obviously, if the real numbers come in higher than expected, it is going to further fan the inflation fears and create more headwinds for the bulls.

Today also brings Consumer Sentiment for April. Looking to next week, it’s another packed calendar for both economic data and earnings. The main data highlights will be the “minutes” from the Fed’s most recent policy meeting, due out on Wednesday, and the March jobs report on Friday, May 3.

Other key reports include the S&P Case-Shiller Home Price Index and Consumer Confidence on Tuesday; ADP’s private payroll report, Job Openings and Labor Turnover Survey (JOLTS), Construction Spending, and ISM Manufacturing on Wednesday; Trade Balance, Factory Orders, and Productivity & Costs on Thursday; and ISM Non-Manufacturing on Friday.

On the earnings front, Wall Street is highly anxious to see results from Amazon on Tuesday and Apple on Thursday. The rest of the week includes results from Domino’s Pizza, NXP Semiconductor, and Welltower on Monday; 3M, ADM, Clorox, Coca-Cola, Corning, Eli Lilly, Gartner, McDonald’s, Mondelez, PACCAR , PayPal, Prudential Financial, Starbucks, Stellantis, Stryker, Super Micro Computer, and Trane Technologies on Tuesday; Aflac, AIG, Airbus, Allstate, Carlyle Group, Carvana, Corteva, CVS, DoorDash, DuPont, eBay, Garmin, Johnson Controls, KKR, Kraft Heinz, Marriott International, Mastercard, MetLife, MGM Resorts, Pfizer, and Yum Brands on Wednesday; Amgen, Cigna, Cloudflare, CNH Industrial, Coinbase Global, ConocoPhillips, Dominion Energy, DraftKings, Ingersoll Rand, Intercontinental Exchange, Moderna, Monster Beverage, Novo Nordisk, Pioneer Natural Resources, Regeneron, Rocket Companies, Shell, The Southern Company, Vulcan Materials, and Zoetis on Thursday; and Hershey and Berkshire Hathaway on Friday.

This week marked the first time we have actually seen money flowing out of Bitcoin ETF's. We have also been seeing money flowing out of mutual funds and other ETF's. The thought is with yields at the bank moving higher, uncertainty about the US economy, and ton of geopolitical unrest brewing money might be looking for safer alternatives with the stock market back near all-time highs.

Big Outflows... for Cathie Wood’s Popular ARK Funds: Investors have pulled a net -$2.2 billion from the six actively managed exchange-traded funds at Cathie Wood's ARK Investment Management this year. Total assets in those funds have dropped -30% in less than four months to $11.1 billion—after peaking at $59 billion in early 2021, when ARK was the world’s largest active ETF manager. Keep in mind, shares of Tesla, the funds largest holding, are down more than -40% this year and trading around $160 per share. Wood has been buying the dip and reiterated her moonshot five-year price target of $2,000 in a CNBC appearance earlier this month. Other top holdings such as Roku, down -33%, and Unity Software, down -44%, have also dragged the fund lower. Remember, Cathie Woods and ARK became a near-overnight sensation in 2020, when the innovation fund posted eye-catching returns and Wood made frequent TV appearances to offer bullish predictions about her top holdings. ARK’s active funds took in $20 billion of new investor money that year, a staggering sum for a small asset manager that made it a darling of the asset-management industry. Wood's, no 68 years old, founded ARK in 2014 in a bid to bring thematic, big-idea investing with a focus on emerging companies to everyday investors. A spokeswoman said ARK’s value creation is evidenced by the flagship fund’s +109% return since its 2014 inception. Source WSJ

Potential CME Competitor Gets Wall Street Backing: Howard Lutnick is lining up some of Wall Street’s biggest power players for a fresh challenge to the behemoth of futures trading and interest-rate derivatives, CME Group Inc. The chief executive officer of Cantor Fitzgerald got backing from Bank of America Corp., Barclays Plc, Citadel Securities, Citigroup Inc., Goldman Sachs Group Inc., JPMorgan Chase & Co., and Jump Trading as he prepares to launch his new futures exchange. The firms invested $172 million for a 25.75% stake in FMX, which increases as they use the platform. The business is part of BGC Group Inc., a brokerage spun off from Cantor Fitzgerald in 2004 and led by Lutnick. By bringing in notable names in finance as investors, Lutnick said he hopes to create value for the venue before it’s even launched. The backers also include Morgan Stanley, Tower Research Capital and Wells Fargo & Co., which signed on to become minority equity owners of FMX, valued at $667 million. Lutnick’s FMX Futures exchange is expected to launch in September, with plans to first list futures linked to the Secured Overnight Financing Rate, or SOFR, a benchmark short-term rate, then Treasury yields. Those futures will compete directly with contracts on CME. Source Bloomberg

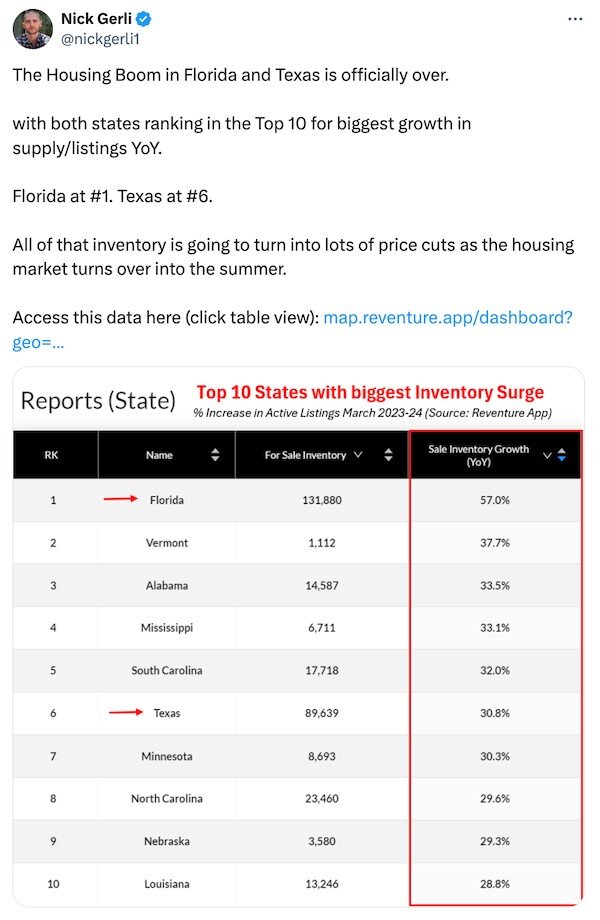

Nearly 40% of Homeowners Couldn’t Afford Their Home If They Were to Buy It Today: Nearly two of every five (38%) homeowners don’t believe they could afford to buy their own home if they were purchasing it today, according to a recent survey by Redfin. The relevant question was: “If you were looking to purchase a home, do you think you could afford a home like yours in your neighborhood today?” Nearly three in five (59%) homeowners who answered this question have lived in their home for at least 10 years, and another 21% have lived in their home for at least five years. That means the majority of respondents have seen housing prices in their neighborhood skyrocket since they purchased their home: The median U.S. home-sale price has doubled in the last 10 years, and has shot up nearly 50% in the last five years alone. Rising mortgage rates are another reason many homeowners couldn’t afford their own home if they were to buy it today. The typical person purchasing today’s median-priced home for $420,000 has a record-high $2,864 monthly housing payment with a 7.1% mortgage rate, the current 30-year fixed-rate average. If they were to purchase a home for the same price with a 4% mortgage rate, which was common in 2019, their monthly payment would be $2,210, roughly $650 less. The fact that buying a bigger, better home–or even a similar home–is financially out of reach for so many Americans is the driving force behind the mortgage-rate lock-in effect. Nearly all homeowners have a mortgage rate below today’s level. Source Redfin |

|

|

|

US Ban on Worker Noncompetes Faces Uphill Legal Battle: The U.S. Federal Trade Commission's ban on "noncompete" agreements commonly signed by workers is likely vulnerable to legal challenges, experts said, as some courts have grown increasingly skeptical of federal agencies' power to adopt broad rules. The commission in unveiling the rule on Tuesday said agreements not to join employers' competitors or launch rival businesses suppress workers' wages and stunt their mobility and job opportunities. About 30 million people, or 20% of U.S. workers, have signed non-competes, the agency said. Business groups led by the U.S. Chamber of Commerce, tax services firm Ryan LLC, and a Pennsylvania tree trimming company have already filed three lawsuits claiming that the FTC, which enforces antitrust laws, lacks the power to determine which business practices amount to unfair competition and should be banned. The Chamber late Wednesday moved to block the rule from taking effect pending the outcome of its lawsuit. Those challenges are likely to delay implementation of the rule, which is set to take effect in August. In the end they may doom the measure, as the FTC has staked out a novel and unprecedented position regarding its rule-making powers, several lawyers and other experts said. Source Reuters

US Fertility Rate Drops to Lowest in a Century: The fertility rate in the United States has been trending down for decades, and a new report shows that another drop in births in 2023 brought the rate down to the lowest it’s been in more than a century. There were about 3.6 million babies born in 2023, or 54.4 live births for every 1,000 females ages 15 to 44, according to provisional data from the US Centers for Disease Control and Prevention’s National Center for Health Statistics. After a steep plunge in the first year of the Covid-19 pandemic, the fertility rate has fluctuated. But the 3% drop between 2022 and 2023 brought the rate just below the previous low from 2020, which was 56 births for every 1,000 women of reproductive age. The birth rate fell among most age groups between 2022 and 2023, the new report shows. The teen birth rate reached another record low of 13.2 births per 1,000 females ages 15 to 19, which is 79% lower than it was at the most recent peak from 1991. However, the rate of decline was slower than it’s been for the past decade and a half. Women 40 and older were the only group to see an increase in birth rate, although – at less than 13 births for every 1,000 women – it remained lower than any other age group. Source CNN

What Are Americans’ Top Foreign Policy Priorities? When asked to prioritize the long-range foreign policy goals of the United States, the majority of Americans say preventing terrorist attacks (73%), keeping illegal drugs out of the country (64%) and preventing the spread of weapons of mass destruction (63%) are top priorities, according to a recent Pew Research survey. Over half of Americans also see maintaining the U.S. military advantage over other countries (53%) and preventing the spread of infectious diseases (52%) as primary foreign policy responsibilities. About half of Americans say limiting the power and influence of Russia and China are top priorities. Notably, fewer than half of Americans say dealing with global climate change (44%) and getting other countries to assume more of the costs of maintaining world order (42%) are top priorities. At the bottom of this list of foreign policy priorities are promoting global democracy and aiding refugees fleeing violence around the world. There are also stark age differences on many of the policy goals mentioned, but for the most part, young adults are less likely than older Americans to say the issues Pew asked about are top priorities. The exceptions are dealing with climate change, reducing military commitments overseas, and promoting and defending human rights abroad . Overall, a majority of Americans say that all 22 long-range foreign policy goals Pew asked about should be given at least some priority. Still, about three-in-ten Americans say supporting Israel (31%), promoting democracy (28%) and supporting Ukraine (27%) should be given no priority. Source Pew Research

PLEASE NOTE: IF YOU ARE A CUSTOMER OF STONE X AS YOUR FCM THEY ARE MIGRATING ALL GAIN PORTAL AND STONE X FUTURES TRADER PLATFORM ACCESS TO A NEW SINGLE LOGIN EXPERIENCE. USE YOUR EMAIL ADDRESS FOR YOUR LOGIN ID . LASTLY IF YOU HAVE NOT ALREADY TESTED THE MY.STONEX.COM PORTAL PLEASE DO SO TODAY AND EMAIL CTG IF YOU HAVE ANY ISSUES NOT STONE X AS THEY TYPICALLY FORWARD US THE EMAILS YOU SEND THEM. THANKS!

|

|

|

Futures trading is speculative and involves the potential loss of investment. Past results are not necessarily indicative of future results. Futures trading is not suitable for all investors.

Nell Sloane, Capital Trading Group, LLLP is not affiliated with nor do they endorse, sponsor, or recommend any product or service advertised herein, unless otherwise specifically noted.

CTG Daily Commentary is published by Capital Trading Group, LLLP and Nell Sloane is the editor of this publication. The information contained herein was taken from financial information sources deemed to be reliable and accurate at the time it was published, but changes in the marketplace may cause this information to become out dated and obsolete.

It should be noted that Capital Trading Group, LLLP nor Nell Sloane has verified the completeness of the information contained herein. Statements of opinion and recommendations, will be introduced as such, and generally reflect the judgment and opinions of Nell Sloane, these opinions may change at any time without written notice, and Capital Trading Group, LLLP assumes no duty or responsibility to update you regarding any changes. Market opinions contained herein are intended as general observations and are not intended as specific investment advice.

Any references to products offered by Capital Trading Group, LLLP are not a solicitation for any investment. Readers are urged to contact your account representative for more information about the unique risks associated with futures trading and we encourage you to review all disclosures before making any decision to invest. This electronic newsletter does not constitute an offer of sales of any securities. Nell Sloane, Capital Trading Group, LLP and their officers, directors, and/or employees may or may not have investments in markets or programs mentioned herein.

|